tataks/iStock via Getty Images

Investment Thesis

Valhi Inc. (NYSE:VHI) is a holding company that owns and operates a web of listed companies, contributing to its earnings. Accordingly, it acts as an investment vehicle with a diversified portfolio of holdings operating in multiple industries. At its core, the company is owned and operated as a family-owned business by the Simmons family with a float of 8.46%, which in my opinion, is in investors’ favor because of a complete alignment of interest.

Its biggest revenue-generating segment is the Titanium Dioxide (TiO2) producing segment operated by Kronos Worldwide Inc. (KRO), one of the largest TiO2 producers in the world, accounting for over 80% of the company’s revenue. Valhi’s earnings are expected to grow sequentially in 2022, in line with KRO’s earnings, after a strong Q1 earnings report.

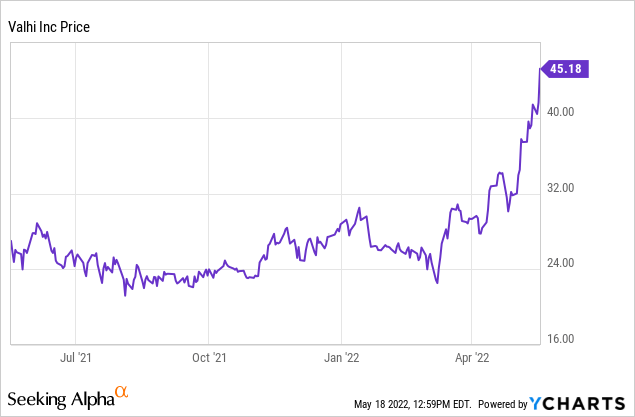

After years of slow movement, the stock has recently surged and doubled since March. Despite Wallstreet’s sell rating on the stock, its valuation metrics are still very desirable, and the long-term aspects appear to be positive.

Company Overview

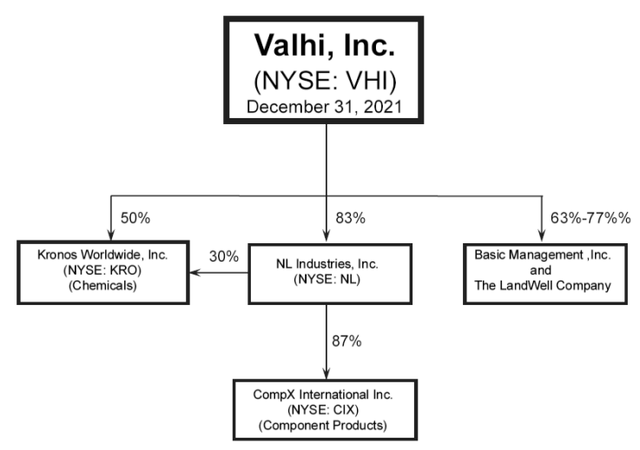

Valhi is a holding company that operates (through its subsidiaries), in the chemical industry through Kronos, component products sector through NL Industries Inc. (NL), which has a controlling interest in CompX International (CIX), and real estate management and development sectors through Basic Management Inc. and The LandWell Company. The company is predominantly controlled by the Contran Corporation, which in turn is controlled by the Simmons family.

Valhi Form 10-K

The chemical division accounted for approximately 84.5%, the component products division for 6.1%, and the real estate division for 9.4% of Valhi’s 2021 annual revenues. Meanwhile, the operating margin was 63% for the chemical, 6.4% for component products, and 30.6% for the real estate segment.

Chemical Segment: Kronos

The largest revenue-generating segment of the company is operated through Kronos, a global producer, and marketer of value-added TiO2 pigments. Kronos has about 4,000 customers in 100 countries across Europe, North America, and the Asia Pacific.

The TiO2 compound is the largest commercially used whitening pigment, also used for brightening, opacity, and durability of various products, including paints, plastics, paper, fibers, and ceramics. It is also a critical component of everyday applications, such as coatings, inks, foods, and cosmetics.

According to Facts & Factors, the global TiO2 market was valued at about $18.8 billion in 2021 and is expected to grow at a CAGR of 5.6% to $27.2 billion by 2028. The automotive industry is one of the biggest customers of TiO2 as a user of associated products and is the primary driving factor for TiO2’s market growth.

About 46% of its annual revenue in 2021 and 48% of revenue in the MRQ came from Europe, the largest growing market of TiO2, where the company claims to have an estimated 15% market share. 37% revenue share in 2021 and 32% in the MRQ came from North America, where its market share is about 17%.

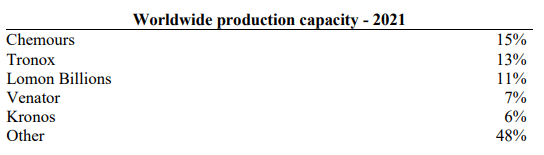

Kronos is the 5th largest TiO2 producer globally, accounting for 6% of the global production.

Kronos Form 10-K

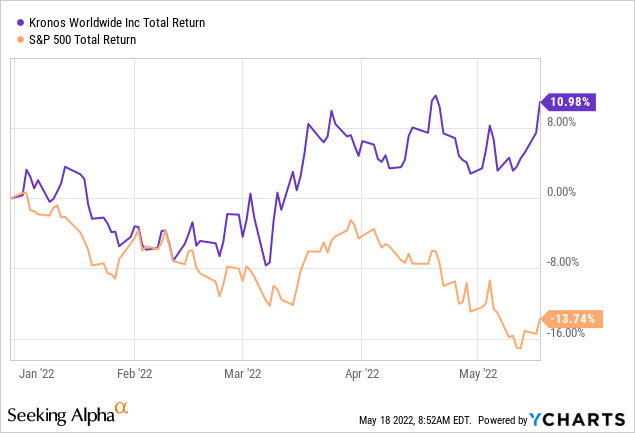

The KRO stock alone has outperformed the market this year with total returns of almost 11%, including a dividend yield of over 4.5%.

Seeking Alpha’s quant ratings have graded the KRO stock as a strong buy because of its strong momentum, upward earnings revisions, growth prospects, and attractive valuation, a substantial improvement from 6 months ago.

Seeking Alpha

TiO2 does not trade on any commodity exchanges, and the prices are set based strictly on negotiations between the suppliers and customers. Because of the recent sales price hikes, KRO’s topline growth has significantly benefited, and its operating income grew by 70% in Q1 2022, aided by a 24% YoY increase in TiO2 prices and a 2% increase in sales volume.

At the same time, Valhi reported a net income of $45.4 million, or $1.59 per share, a threefold increase compared to the previous year, primarily attributable to the high operating income generated by Kronos.

I expect its growth to continue throughout the year and its EPS to grow in line with the expected sequential growth throughout 2022, positively influencing Valhi’s earnings. As an individual investment, KRO is a good dividend stock, whereas, Valhi leverages KRO as an earning source to deleverage itself and aid capital appreciation.

Valuation

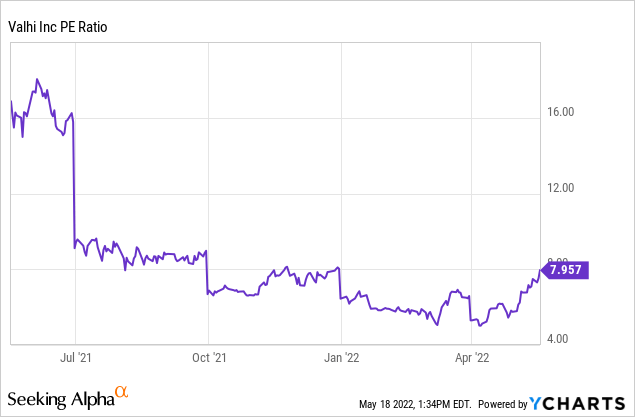

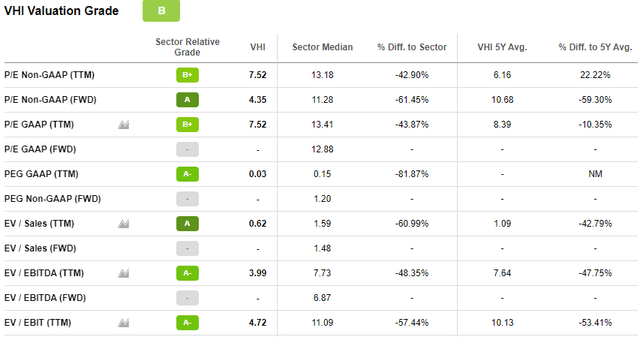

Valhi is not trading at a ludicrous valuation multiple despite the recent surge. In fact, the company is trading at a PE of approximately 43% lower than the industry median and 10% lower than its 5-year average. This tells us that even though the PE is higher than it has been for most of the year, it’s still lower than it could be, and it’s still not too late to invest in the stock.

Based on its current metrics and its 5-year averages, the company should be trading at around $75, an upside of over 70%. If we use the industry median, the value goes further up, but since the stock has historically traded below industry medians, it wouldn’t be meaningful to use those numbers.

Seeking Alpha

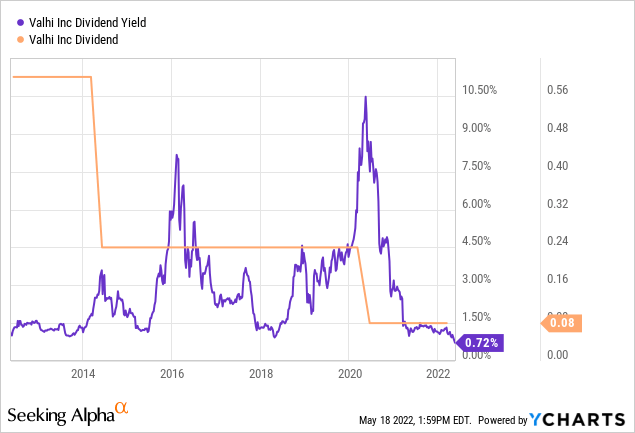

Additionally, as an added benefit, the company also disburses a dividend, yielding 0.77%. It’s considerably lower than its 4-year average yield of 3.37% because of the price surge but is amply covered by its free cash flow yield of over 26%.

Valhi has a 27 years history of consecutive dividend payouts but slashed its dividend by 60% in 2016 and then by two-thirds in 2020.

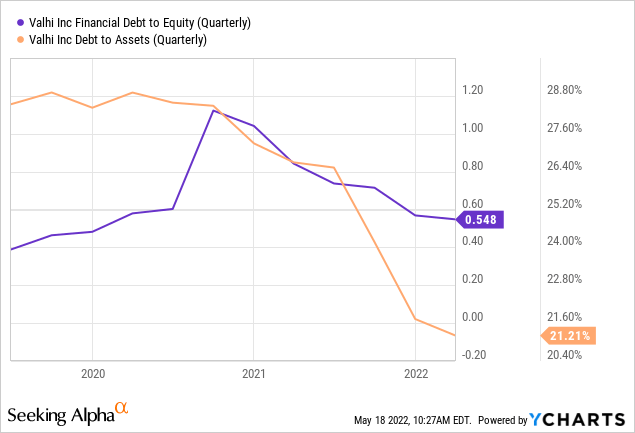

Since then, the company has grown its book value from negative $1.27 to $31.12 in the MRQ, tangible book value per share from negative $14.70 to $17.69, and the total debt has gone down from $810 million to $662 million. So the company is in a much stronger position, and a dividend raise shouldn’t be off the table because of the solid annual free cash flow yield.

Conclusion

Valhi stock has gained about 51% YTD and doubled since it released its Q4 earnings report, implying its high sensitivity to positive market sentiment. The rising prices which have aided its Q1 financial reports are expected to continue throughout the year, and I expect the positive momentum to aid in the stock price to reach the levels last seen in 2018.

I haven’t touched on the remainder of its businesses in the article because of the heavy footprint that the chemical segment has on VHI’s financials. Investors looking for a solid income stock would be better off further researching and monitoring the KRO stock.

The valuation metrics have embossed the VHI stock with a material upside potential for investors who can stomach the volatility because stocks which are sensitive to bullish market signals are also sensitive to bearish signals. Therefore, the stock is a long-term buy-and-hold investment rather than a short-term trading vehicle.